Content

This decision will depend on when your business recognizes its revenue and expenses. Bookkeeping traditionally refers to the day-to-day upkeep of a business’s financial records. Bookkeepers used to simply gather and quality-check the information from which accounts were prepared. But their role has expanded over time, and we’ll look at how in the next chapter. Get your small business’ bookkeeping off on the right foot with banking tools that make transacting simpler than ever to manage. Let NorthOne help you open a business bank account that’s easily integrated into your bookkeeping software, so you always have the financial transparency needed to succeed.

Balance SheetA balance sheet is one of the financial statements of a company that presents the shareholders’ equity, liabilities, and assets of the company at a specific point in time. It is based on the accounting equation that states that the sum of the total liabilities and the owner’s capital equals the total assets of the company.

Account

Bookkeeping is the process of recording your company’s financial transactions into organized accounts on a daily basis. It can also refer to the different recording techniques businesses can use. Bookkeeping is an essential part of your accounting process for a few reasons. When you keep transaction records updated, you can generate accurate financial reports that help measure business performance. General LedgerA general ledger is an accounting record that compiles every financial transaction of a firm to provide accurate entries for financial statements.

What balance sheet means?

A balance sheet is a financial statement that contains details of a company's assets or liabilities at a specific point in time. It is one of the three core financial statements (income statement and cash flow statement being the other two) used for evaluating the performance of a business.

Post adjusting journal entries at the end of the period to reflect any changes to be made to the trial balance run in Step 3. The history of accounting has been around almost as long as money itself. Accounting history dates back to ancient civilizations in Mesopotamia, Egypt, and Babylon. For example, during the Roman Empire, the government had detailed records of its finances. Bookkeepers might also perform tasks that use technology to streamline accounting tasks such as accounting programs or spreadsheet software. In order to stay current in a virtual environment, bookkeeping can typically require the application of technological skills along with the skills essential to accounting. A bookkeeper might be responsible for managing the tax, benefits and other deductions of employee wages to ensure the accuracy of payroll processing and documentation.

Bookkeeping Definition

Bookkeeping is the process of tracking and recording a business’s financial transactions. These business activities are recorded based on the company’s accounting principles and supporting documentation. Unlike the journal, ledgers are investigated by auditors, so they must always be balanced at the end of the fiscal year. If the total debits are more than the total credits, it’s called a debit balance. If the total credits outweigh the total debits, there is a credit balance.

It ensures the owner by providing the actual record of all company’s economic activities to avoid further conflicts. Small companies that may be looking to be acquired often need to present financial statements as part of acquisition or merger efforts. Instead of simply closing a business, a business owner may attempt to “cash-out” of their position and receive compensation for building a company. Bookkeepers may also assist in the preparation and filing of a company’s income taxes. Tax preparation could include organizing financial records for filing tax statements, entering data into tax preparation software and reporting revenue, expenses and other deductions. Bookkeeping can involve a wide variety of tasks that serve important functions in maintaining a business’s financial records. From recording sales revenue to balancing accounts, bookkeeping can commonly include the following tasks.

Introduction to bookkeeping

The accounting process includes summarizing, analyzing, and reporting these transactions to oversight agencies, regulators, and tax collection entities. The financial statements used in accounting are a concise summary of financial transactions over an accounting period, summarizing a company’s operations, financial position, and cash flows. Bookkeeping involves keeping track of a business’s financial transactions and making entries to specific accounts using the debit and credit system. Every accounting system has a chart of accounts that lists actual accounts as well as account categories. There is usually at least one account for every item on a company’s balance sheet and income statement. In theory, there is no limit to the number of accounts that can be created, although the total number of accounts is usually determined by management’s need for information. Bookkeeping is the recording of financial transactions, and is part of the process of accounting in business and other organizations.

- Purchase ledger is the record of the purchasing transactions a company does; it goes hand in hand with the Accounts Payable account.

- Cash registers also store transaction receipts, so you can easily record them in your sales journal.

- The financial statements are essential to secure the financial health of small and large businesses.

- Here, every transaction must have at least 2 accounts , with one being debited & the other being credited.

- As a child, I had a neighbor who died at the age of 75, leaving records that accounted for every penny of their income and expenditures since their 21st birthday.

- Records were made in chronological order, and for temporary use only.

So, to reduce the mismatching of each entity, there are few tools or software available, including cloud accounting solutions, income spreadsheet templates, etc. So, assimilating personal and professional expenses is a bad idea and creates a stressful life for all businessmen. The first and foremost step for starting your journey towards Bookkeeping is separating the personal and professional expenses from each other. The Securities and Exchange Commission has an entire financial reporting manual outlining reporting requirements of public companies. Prepare the adjusted trial balance to ensure these financial balances are materially correct and reasonable. Tax accountants overseeing returns in the United States rely on guidance from the Internal Revenue Service. Federal tax returns must comply with tax guidance outlined by the Internal Revenue Code .

Account Balance

Bookkeeping is a process through which a company or an organization keeps a record of a company’s financial transactions by entering the details into a physical book or accounting software. Bookkeepers assist a company with the documentation of the financial operations resulting what is bookkeeping from any sort of business activity. A bookkeeper is a professional who manages a business’s financial transactions and recording. With an efficient bookkeeper, a business can ensure accurate and efficient recording and management of its financial assets and liabilities.

Instead of collecting cash at the time of an agreement, it may give a customer trade credit terms such as net 30. Without accounting, a company may have a hard time keeping track of who owes it money and when that money is to be received. The difference between these two accounting methods is the treatment of accruals. Naturally, under the accrual method of accounting, accruals are required. Under the cash method, accruals are not required and not recorded. Financial accounts have two different sets of rules they can choose to follow.

Bookkeeping – Definition, Importance, Types & Methods

Different businesses have different kinds of payroll setup and the process. In addition, it is also important here to make sure you pay all your dues on time. There are two Bookkeeping methods are available in the business industry, and they’re single-entry and double-entry Bookkeeping. Investopedia requires writers to use primary sources to support their work. These include white papers, government data, original reporting, and interviews with industry experts.

- Column One contains the names of those accounts in the ledger which have a non-zero balance.

- Net LossNet loss or net operating loss refers to the excess of the expenses incurred over the income generated in a given accounting period.

- Because of the simplified manner of accounting, the cash method is often used by small businesses or entities that are not required to use the accrual method of accounting.

- Larger companies often have much more complex solutions to integrate with their specific reporting needs.

- Your bookkeeping is further used to prepare different financial statements such as balance sheet, income statement, etc.

- Is a method whereby only the financial transactions facilitated through money exchange can appear in the books.

Amanda Bellucco-Chatham is an editor, writer, and fact-checker with years of experience researching personal finance topics. Specialties include general financial planning, career development, lending, retirement, tax preparation, and credit. When intelligently used, accounting records warn of impending financial difficulties or even insolvency. As a child, I had a neighbor who died at the age of 75, leaving records that accounted for every penny of their income and expenditures since their 21st birthday. Bookkeeping today is likely to be done with the aid of a computer rather than with handwritten books, and this is a virtual certainty in a business of any size or significance. Further, financial software is often more feasible and faster than hiring bookkeepers.

Cash accounting is a hand-in-hand transaction where the ledger is not involved until the cash is submitted into bank accounts. Another critical decision to create Bookkeeping is to choose between cash accounting and accrual accounting. The documentation might be a receipt, a purchase order, an invoice. It can be any other financial record similar to it that confirms that the transaction took place. Bookkeeping transactions https://www.bookstime.com/ can be recorded manually in a journal or by using a spreadsheet program like MS Excel. Without insight into how a business is performing, it is impossible for a company to make smart financial decisions through forecasting. Without accounting, a company wouldn’t be able to tell which products are its best sellers, how much profit is made in each department, and what overhead costs are holding back profits.

- If you’re looking to convert from manual bookkeeping to digital, consider a staggered approach.

- The reports generated by various streams of accounting, such as cost accounting and managerial accounting, are invaluable in helping management make informed business decisions.

- We believe that Bookkeeping and accounting is a very important part of every business.

- Categorizing the transactions under the books requires many processes, and the subcategories of accounts such as liabilities, revenue, assets, and expenses need to be organized smartly.

- There are two Bookkeeping methods are available in the business industry, and they’re single-entry and double-entry Bookkeeping.

- Bookkeeping involves the recording, on a regular basis, of a company’s financial transactions.

However, the balance sheet is only a snapshot of a business’ financial position for a particular date. Record all your business’s transactions and separate them into categories. The bottom line is that bookkeeping provides an organized look at a business’ finances, which makes it easier to answer key accounting questions. Bookkeeping provides the crucial financial data necessary to answer these questions and more. Your bookkeeping is further used to prepare different financial statements such as balance sheet, income statement, etc. It is also important to ensure here that all your documents are stored and well organized as well as easily accessible for all the team members or consultants who are supposed to use them.

Cash Basis

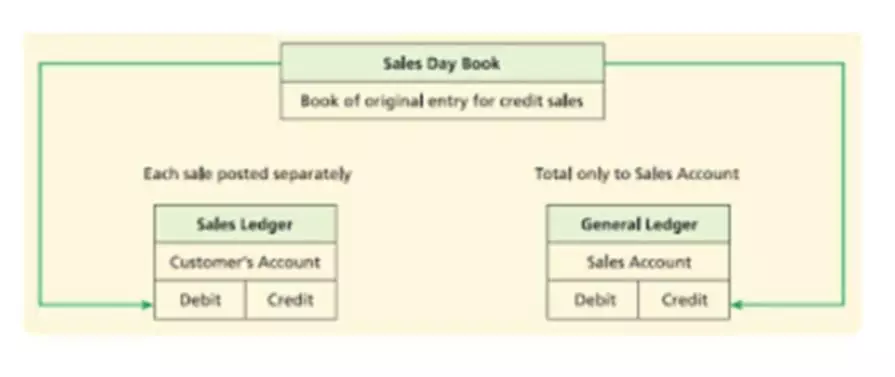

Not only can this help you set goals, but it can also help you identify problems in your business. With an accurate record of all transactions, you can easily discover any discrepancies between financial statements and what’s been recorded. This will allow you to quickly catch any errors that could become an issue down the road. Without bookkeeping, accountants would be unable to successfully provide business owners with the insight they need to make informed financial decisions. As you can see, bookkeeping is only a small part of the broader definition of accounting. Sales ledger, which deals mostly with the accounts receivable account.

- BookkeepersAccountantsThey generally have on-the-job training experience.

- In single-entry bookkeeping, every transaction has just one entry; in double-entry bookkeeping, every transaction has both a debit and a credit.

- Keeping accurate records of every transaction allows business owners to see, at a glance, if they’re bringing in more money than they’re paying out.

- Posting is the process by which account balances in the appropriate ledger are changed.

- It allows you to understand how well your company handles debt and expenses.

- Without accounting, investors would be unable to rely on timely or accurate financial information, and companies’ executives would lack the transparency needed to manage risks or plan projects.